Aangemaakte reacties

-

AuteurBerichten

-

The “Money Supply” with a Gold Standard 2 : 1880 – 1970

by Nathan Lewis – New World Economics

Originally published January 11th, 2011Last week, we were looking at how gold standard systems work. We used the example of the United States, which, from 1789 to 1860, had a libertarian “free banking” system. Anyone could issue currency, but it had to be pegged to gold. This “gold peg” was a value peg. It had nothing to do with gold mining, or the gold reserves of banks, or imports and exports of gold. Does gold mining alter the value of gold? Essentially no, because annual gold mining production is a small fraction — about 2% — of existing world gold supply. Does importing and exporting gold change the value of gold? Not unless there are some sort of restrictions on importing and exporting, which is rare, and hard to enforce even if it exists. Gold is the same value everywhere. Does the fact that a bank owns or does not own gold change the value of gold? Nope. It’s the same value no matter who owns it. So you see, none of these factors have much effect on the value of gold. And if a banknote’s value is pegged to gold — via the adjustment of supply — then obviously these factors have little effect on the value of banknotes.

The fact of the matter is, during the “free banking” period, nobody actually knew what the “money supply” was. In 1859, the Hodges Genuine Bank Notes of America listed 9,916 notes issued by 1,356 banks. Yes, there were 1,356 banks all issuing their own homegrown currency in those days, all of it linked to gold. Actually, there were more than 1,356 banks, because Hodges missed dozens if not hundreds of banks! Banks were opening and closing all the time. Do you see? Not only did nobody know the total amount of banknotes in issuance (except for some vague statistics), nobody even knew how many banks there were issuing currency. Think about that. So how was the money supply determined in those days? All of these 1,356+ banks had the same operating mechanism, which was a gold value peg maintained via the adjustment of supply. When the value of banknotes was a little low compared to its gold peg, the supply of banknotes was reduced. When people were happy to accept larger issuance of banknotes, without redeeming them for gold, in other words when the value of banknotes was higher than the gold peg, then the supply of banknotes increased.

January 2, 2011: The “Money Supply” With a Gold Standard

August 26, 2007: How To Operate a Gold Standard

August 19, 2007: Gold Standard FallaciesUnfortunately, today we have all sorts of the stupidest imaginable ideas floating around, whereby a “gold standard” is a system by which the amount of money in circulation is determined by gold mining, or the “current account balance,” or that a gold standard means a “100% gold reserve ratio” or absolutely no change in the “money supply” whatsoever, some such thing. Anyone with the briefest understanding of historical monetary statistics — this includes you if you read last week’s item — can see immediately that this is complete baloney. The next thing you should realize is that 99% of academic economists including Ben Bernanke and also 95% of gold standard advocates including Murray Rothbard — also have no idea whatsoever how real gold standard systems operated, in real life during the period 1789-1971. What this means is that, after spending 20 minutes to read last week’s item, you now know more about this than 95%+ of the so-called “experts.” Do you see now why I say that today’s understanding of these matters is appalling? On the other hand, you can now be a World Expert with about 45 minutes of work. Which is sort of fun, in a way.

Let’s continue our story in 1880. In 1863, the National Bank Notes system was introduced in the United States. Banks that wanted to issue currency had to register with the Office of the Comptroller of the Currency, an agency of the U.S. Treasury. There were still thousands of these National Banks — 3,438 National Banks in May 1890 — so it was still a libertarian sort of system. However, now we have system-wide statistics on the total banknotes outstanding. The dollar floated vs. gold from 1861 to 1879, so 1880 is a good place to restart our tale of how the gold standard system operated in the United States. The National Banks themselves didn’t hold gold reserves for the most part, but rather U.S. Treasury obligations. The gold reserve of the National Bank system was the U.S. Treasury itself.

Here is some information on the National Bank system from the annual reports of the OCC:

http://fraser.stlouisfed.org/publications/comp/

The St. Louis Fed has all kinds of wonderful historical stuff. You used to have to go to the library for this sort of thing. I did a lot from microfilm! Ugh.

Unfortunately, I don’t have good statistics on U.S. Treasury gold holdings from 1900 to 1913. I only have 1905 and 1910. So, the intervening years are linearly extrapolated. If you have these numbers, let me know.

Let’s review first the history of the dollar.

The “dollar” was originally a European silver coin called the “thaler.” It originated in 1518. This became the Spanish silver “dollar,” which became the template for the U.S. dollar when the dollar was defined in 1792. So, the idea of the “dollar/thaler” goes waaaay back.

Except for a minor adjustment in 1834, the dollar’s value was unchanged until the Roosevelt devalutation in 1933. We can consider the entirety of the 1789-1932 period as having a dollar pegged to gold at $20.67/oz. There was a lapse during the Civil War, and also some business around the War of 1812. After the Roosevelt devaluation, the dollar was pegged at $35/oz., until 1971. However, there were some lapses during this time too, especially during World War II.

Here you can see the Civil War devaluation and return to the gold standard, the 1933 devaluation, and the floating currency period after 1971.

This shows the WWII “lapse” in the gold standard — the U.S. wasn’t quite off gold, but not quite on it either, it was all a little fuzzy, hey, there was a war going on — and the return to the $35/oz. peg around 1952, after the “Fed Accord” of 1951. The dollar sank to about $43.25/oz. at its lowest point in 1948, which is to say that it took 43.25/35=23.5% more dollars to buy an ounce of gold, or in other words the dollar’s value fell by 19%. Not really that big a deal, as long as it didn’t get out of hand.

There you go. The pink bars are base money (not including gold coin), basically banknotes and bank reserves. The green bars are the total amount of gold held by the U.S. Treasury, in terms of dollars. You can see a big jump in gold reserves in 1934, because that’s when they were revalued at $35/oz. instead of $20.67/oz. The data comes from Milton Friedman A Monetary History of the United States, “high powered money” minus gold coin, which comes from the Federal Reserve’s Banking and Monetary Statistics. The base money figues after 1918 come from the St. Louis Fed.

During this period, base money expanded by 90x. If you adjust for the 1933 devaluation, the expansion in the “gold value of the money supply” is 53x. Does that sound to you like “no expansion in the money supply”? During this period, 1880-1970, the total amount of gold in the world rose by 6.51x. So you see, the money supply with a gold standard has nothing to do with gold mining, imports or exports of gold, the current account balance, “no expansion in the money supply,” “100% reserves” or some other stable reserve ratio, or all the other stupid things you hear about all the time.

Twee interessante stukjes over Goud getipt door Rob.

Gold Outlook 2011: Irreversible Upward Pressures and the China Effect

I know this may appear to some to be an enviable job—getting to speak about the one asset class that seems to continually out-perform all others year after year—but it is a double edged sword.

I’ve struggled to find an appropriate simile. The best I can come up with is that speaking about gold is like one of those good news bad news jokes, you know the ones—your doctor phoned with some good news and some bad news. The good news is they will be naming a new incurable disease after you.

The good news is that gold is rising in value; the bad news is—well nearly everything else about the economy.

This year we travelled to the Middle East, the Far East and South and Central America to discuss gold. The different mindsets about gold we encountered there surprised all of us. Most people in these countries see gold as the protector of wealth. In the West, we view gold as a commodity for speculation.

Western economists treat the act of buying gold as an admission of defeat and their attempts at disparaging gold’s steady rise became even more tenuous than ever this past year. Some of these disparaging opinions include:

“Financial tightening will cause commodity prices to fall.”

“Gold is in a bubble.”

“The gold stocks haven’t confirmed the gold bull.”Perhaps most desperate of all—“The economy is on the road to recovery.”

Despite these protests, gold had another remarkable year. It was up 25 percent in 2010, which marked its tenth straight annual gain.Although we are speaking about gold today, I would be remiss in ignoring silver’s performance. Silver is up 78 percent in 2010 as it is, like gold, beginning to assume its role as a monetary metal. Platinum was also up 17 percent.

When we look at a ten year chart of the US and Canadian dollars, the Euro, the British Pound and the Yuan, we see that these five major currencies have lost between 70 to 80 percent of their purchasing power against gold over this 10 year period. In truth, gold is not rising, currencies are falling in value and gold can therefore rise as far as currencies can fall.

Three Short to Mid-Term Trends

I’d like to pick up where we left off last year with a review of three dominant medium term trends that put upward pressure on the price of gold in 2010 and will likely continue to in 2011. Then I’d like to look briefly at three longer term, irreversible trends that will to put downward pressure on currencies resulting in upward pressure on gold for decades.

First, the three dominant mid-term trends we discussed last year. These are:

1. Central Banking Buying

2. Movement away from the US Dollar

3. ChinaCentral Bank Buying

In 2009, for the first time in 20 years, monetary gold, or central bank and investment buying, outpaced gold buying for industrial or jewellery purposes. In 2010 China, Iran, Russia and India’s central banks were all significant buyers as they moved cash reserves to gold.

In Q3 of 2010, Russian central bank gold holdings rose seven per cent to 756 tonnes. In 2010, the Russian Central Bank bought 2/3 of its own gold production.In December we learned that China had imported 209.7 metric tonnes of gold in the first 10 months of the year. This was a 500 percent increase over the same period of 2009 and on top of their world leading domestic gold production.

By the third quarter, India’s gold imports, both commercial and private, for the year were 624 tonnes, putting them 100 tonnes above the previous year’s total of 595 tonnes. Fourth quarter purchases could put India’s annual total over 750 tonnes.

China and Russia need to acquire gold to bring their gold reserve ratio to outstanding currency closer to Western central banks. Russia needs to acquire at least 1000 tonnes and China at least 3000 tonnes to remain on parity with the US. Chinese officials have stated publicly that China would like to acquire at least 6000 tonnes. Unofficially they have stated targets as high as 10,000 tonnes.

Movement Away from US Dollar

Last year we quoted a November 2009 story written by veteran journalist Robert Fisk claiming Russia and China along with France, were working on an agreement to trade oil with Arab states using currencies other than the US dollar. As expected, central bankers fervently denied these rumours. The US dollar has since 1973 been the only currency that oil could be traded in. This is the only reason the US has been able to amass nearly $14 trillion in debt. Loss of the petrodollar`s hegemony would have a devastating effect on the US as this is essentially the only reason foreign countries in the past needed to hold US dollars.

On November 24, 2010, China and Russia officially

quit the dollarand agreed to use each other’s currencies for bilateral trade—including oil. Official trading on Moscow’s MICEX Index began December 15th, 2010.In 2009, Robert B. Zoellick, made his well-publicized comment that, the US would be “. . . mistaken to take for granted the dollar’s place as the world’s predominant reserve currency.” And that, “. . . looking forward, there will increasingly be other options to the dollar.” In 2010 he continued hinting at a new reserve currency made up of five currencies with gold as the “reference point.” He also called for a new Bretton Woods agreement this year. Mr. Zoellick is no lunatic goldbug. He’s the President of the World Bank.

China

Last month, I was a speaker and panellist at the China Gold and Precious Metals Summit in Shanghai. I can confirm that Chinese buying, both official and public, is a major trend that is not only well in place, but may be the single most important influence on the price of gold in 2011. As I said, the Chinese see gold quite differently from the way we see it. If we are to understand gold’s price direction in 2011 and beyond I believe it is essential to understand the “mindset” the Chinese have built around gold.

Economic Mindsets and Gold

Although the forming of economic mindsets is a complex topic, I’d like to simplify how major financial mindsets are created in one sentence. What our government, our banks and financial media tell us about money is what most of us will accept as our financial mindset or financial reality. If anyone doubts the power of government economic policy to shape mass economic reality, just look at how we have changed our attitudes towards debt, saving and economic value over the past 40 years. Our current debt based mindset began to form the day the US dollar, the worlds reserve currency, was removed from its final international peg with gold in 1971.

Different Attitudes about Gold

Although the West shares many common economic principles with the East, as the capitalist banking systems are similar, there is one area where there is a clear distinction—this is how Easterners view the role of gold as money.

Western governments fear gold. It restricts their ability to create currency

In the West, governments borrow and encourage their constituents to follow their example. Banks encourage us to borrow for everything from vacations to widescreen televisions made in China. They tell us we are “stimulating” the economy through consumption. Generally speaking, the investing public in the West sees gold as a wealth gaining asset to be traded like stocks and bonds. This is why Westerners are constantly fretting about the price of gold in currency terms.

The Chinese government, on the other hand, respects gold. This is evident by the laws they have passed to facilitate mining and private gold ownership. China currently leads the world in gold production.

The government encourages the public to put 5 percent of their savings—yes they encourage savings—into gold. This is significant because the Chinese can save up to 40 percent of their annual salary. In the West, most middle class families are lucky to break even. The Chinese see gold as a wealth preserving asset that will weather all seasons. This is the difference that I believe anyone who wishes to fully understand gold’s rising price must comprehend. Inhabitants of older countries, who have lived through the destruction of an inflation fuelled currency crisis, do not need to be reminded that gold is the most effective hedge against inflation and a currency crisis.Former CEO of Newmont Mining, Pierre Lassonde also feels that it will be buying by the Chinese public that will eventually propel gold prices into the stratosphere.

Three Irreversible Trends

Clearly, the three medium term trends we noted last year are still firmly in place. Now I’d like to look at three longer irreversible trends that I believe will affect the price of gold and currencies for decades. These are:

1. The aging population.

2. Outsourcing

3. Peak oilThe Aging Population

The aging population is a combination of a population that is living longer and the “pig in the python” effect of a huge tidal wave of “baby boomers” born between 1946 and 1963 who are just starting to enter retirement age. As people age, they spend less and downsize. GDP and tax revenues are reduced and a much smaller workforce follows the baby boomers so this is a triple whammy. This problem is universal. In China, it is further exacerbated by their one child per couple policy. Governments will have no choice but to create more currency and further debase it.

Outsourcing

Outsourcing has almost entirely destroyed the manufacturing sectors of many first world countries like the US and Canada and much of Europe. The Chinese worker who built your IPhone made $287 a month; this was after a well-publicized raise. The West simply can no longer compete with these labour costs. The United States was the world’s largest manufacturer after WWII and has driven the world’s economy ever since. However, the US consumer can no longer buy things as they lose their jobs. As factories move off shore the high unemployment becomes systemic. Without jobs, the GDP and the tax revenues of the US fall. The mountain of federal, state and municipal debt will become even harder to service and the government will be forced to go even deeper in debt and to further debase its currency.

Peak Oil

Peak oil is the point at which the maximum rate of global petroleum extraction is reached, after which the rate of production enters terminal decline. This has already happened in the US, Alaska and the North Sea. In the next few years Mexico will become an importer of oil and the US will lose its third largest supplier. Our fragile, highly indebted economy relies on this land based cheap oil to continue and it cannot withstand the shock of transitioning to more expensive alternatives. In September of 2010 a German military think tank reported that the German government is taking the threat of peak oil seriously and preparing accordingly. Numerous studies around the world have concluded that we are very close to peak oil production, which will be accelerated due to gulf drilling bans.

This will lead to higher price inflation for most goods. This will be another blow to the fragile US economy, which currently pays less for oil and gas than any of the first world countries. When added to the effects of the waning strength of the petrodollar the results will be devastating.

May I remind you that if China, which currently has one tenth the number of cars per capita as Americans, was to reach par with the US, we would need, by one estimate, seven more Saudi Arabia’s to meet their needs.

These three mega trends will continue to lower the GDP, lower the tax revenue, create higher trade deficits, create higher unemployment, resulting in the need for further currency creation. This will cause inflation to rise as currencies depreciate in value and create higher universal debt. All of this means the gold price will continue to rise.

Competition for the World’s Gold

Finally, as a direct result of world-wide debt and currency debasement, more people will be competing for the world’s available gold. We discussed peak oil, but gold is also reaching a peak as fewer and fewer new deposits are being found. Smaller, lower grade deposits with none of the “economy of scale” benefits of larger deposits are being put into production out of desperation. Mine supply has been in a decline since 2000.

As safe haven demand accelerates, there will be a transition from the $200 trillion of financial assets to about the $3 trillion of above ground gold bullion. Of the $3 trillion of above ground gold bullion about half is owned by central banks and half is privately held. The privately held gold is largely held by the world’s richest families and is not for sale at any price. The central banks are now net buyers. If the world’s pension funds and hedge funds moved only five percent of their assets into gold, which these days seems quite conservative, gold would trade above $5,000.

So in conclusion, I will say that without any new financial crisis, both mid-term and long term trends are in place to ensure gold and silver will continue rising through 2011 and well beyond. For those of you who are looking for a prediction…last year at the Empire Club, I forecast that the price of gold to be between $1300 and $1500 at the end of 2010. We ended up right in the middle at $1405. For 2011, I recently forecast it may climb to $1,700 to $2000 per ounce based on the last five years performance and the factors I have presented today.

I encourage you to follow the example of those who know how devastating a currency crisis can be and buy gold to protect wealth and not treat it as speculation. I’d like to close with a quotation that seems to put all of this into perspective. It comes from Norm Franz’s appropriately titled book, Money and Wealth in the New Millennium. He said,

“Gold is the money of kings; silver is the money of gentlemen; barter is the money of peasants; but debt is the money of slaves.”Thank you.

Vincent, je “vervuilt” deze draad niet, sterker nog: het is leuk als iedereen zijn steentje bijdraagt zodat het een actieve discussie wordt.

UBS Sees Silver Hitting $35 On “Physical Interest In The Metal”

It took just three months (and a 50% spike in price) for UBS to do a 180 on silver. In the firm’s most recent Silver update from Dominic Schnider of Wealth Management Research, the author now says “Silver prices remain well supported and have been able to trade repeatedly above USD 30/oz.” More importantly for those who are concerned that the recent all time high just north of $31 was a one time fluke, fear not: “Temporarily, prices could even hit USD 35/oz on physical interest in the metal due to firm economic activity.” Bottom line: “Investors should make use of silver volatility for yield enhancement strategies At levels close to USD 25/oz, we are willing to pick up the metal.” Then again, none of this should come as a surprise or even lead one to make investment decisions: after all it was just in September that the same person, in a report titled: “Price strength not on firm ground” said “We expect industrial demand to show some weakness and advise investors to avoid the metal” and concluded “We therefore prefer to be sellers at present levels and would reopen a position at or below 17.5/oz.” Merely another confirmation that virtually every sellsider on Wall Street is merely a momentum riding, backward looking, chart monkey, and all those who seek original, contrarian thought are advised to stay very, very far from Wall Street “analysis.”

From the most recent Schinder report:

* Silver prices remain well supported and have been able to trade repeatedly above USD 30/oz.

* Temporarily, prices could even hit USD 35/oz on physical interest in the metal due to firm economic activity.

* However, if 2004-2008 is a performance indicator, the persistent outperformance of silver versus gold should come to an end.he re-rating of silver looks completed – for now Silver prices appreciated more than 80% in 2010. With the rebound in economic growth, we estimate fabrication demand grew by more than 15% last year. Strong silver imports by China and Japan are a reflection of higher silver use. The role of China as a persistently large net importer is rather new. For 2010, net imports should have soared to almost 3,500 tons. This is 50% more than before the financial crisis. With fabrication demand returning, the supply and demand balance has begun to tighten up. Since investment demand has been strong as well, the gold-silver ratio swiftly reached 45 – similar to 2004-2008.

If the term structure of US interest rates remains a good predictor of economic activity and history repeats itself, the gold-silver ratio should lack a directional trend in the coming quarters. This suggests the re-rating is completed, which is largely reflected in our forecast. Risk to our view relates to the industrialization of large emerging market countries, like China and India, which is fully under way. Coupled with heightened fears on public debt monetization in the developed world and the lack of market depth, the gold-silver ratio could drop – over time – into the 30-45 range like in the 1970s.

Recommendation

Investors should make use of silver volatility for yield enhancement strategies At levels close to USD 25/oz, we are willing to pick up the metal.

http://www.zerohedge.com/article/ubs-sees-silver-hitting-35-physical-interest-metal

Manipulatie van de Zilverprijs? En kopen de Chinezen zilver?

The Silver Bears Are Back For Round Three, Explaining Two Key Recent Developments In The World Of Silver

Part 3 – Silver Manipulation Explained

Cyclustheorie: lopen we wel in een rechte lijn?

Try as you might, you can’t walk in a straight line without a visible guide point, like the Sun or a star. You might think you’re walking straight, but as NPR’s Robert Krulwich reports, a map of your route would reveal you are doomed to walk in circles.

Kijktip voor vanavond: Jim Rogers en Arianna Huffington in Tegenlicht: Agenda 2011.

Maandag 10 januari 20:55 NED2

De economie flink in het rood, de politiek hopeloos gepolariseerd en de wereld weer ouderwets verdeeld. Hoogste tijd voor nieuwe inspiratie. Zoals elk kalenderjaar ging Tegenlicht ook in november en december 2010 weer op zoek naar zijn ‘tijdgeestverwanten’. Om de vooruitzichten te peilen voor het jaar 2011, en daar voorbij: het decennium ‘jaren ’10’. De speurtocht in de wereld van wetenschap, economie, futurologie en nieuwe media resulteerde in vier tegendraadse en vernieuwende doordenkers. Voorgangers naar een hoopvoller toekomst. Misschien wel pioniers van een nieuw paradigma.

Superinvesteerder en grondstoffenguru Jim Rogers ziet de wereld steeds meer worden zoals hij altijd voorspelde. Daarom is zijn laatste voorspelling uit Agenda 2009 nu wellicht actueel: ‘It is going to get worse’. Jos de Putter ontmoet oude bekende Rogers in Newark, in transit tussen twee vluchten. Rogers pendelt heen en weer tussen de VS en Azië, waar het volgens hem nu allemaal aan het gebeuren is. Europa kan hij gevoeglijk overslaan. Want hij voorspelde in 1999 namelijk al de val van de Euro. Want de Europese economieën zijn te divers, er is geen eenheid in de politiek en vooral: ‘’they are faking the numbers’.

http://tegenlicht.vpro.nl/afleveringen/2010-2011/agenda-2011.html

Eigenlijk is het de schuld van Nixon in 1971. Die heeft de goudstandaard verlaten. Dit kwam doordat hij nogal wat geld nodig had voor de oorlog in Vietnam.

Dus is hij meer geld gaan bijdrukken dan dat er goud was. Nu is het hek van de dam. Wat er nu de Amerika gebeurd is onomkeerbaar.

Op naar de HYPERINFLATIE.

Als we nu weer al het geld willen afdekken met GOUD. Waar zal de goudprijs dan naar toe gaan?

Lees ook stukje over Bretton Woods op Wikipedia.

Auteur: Rob

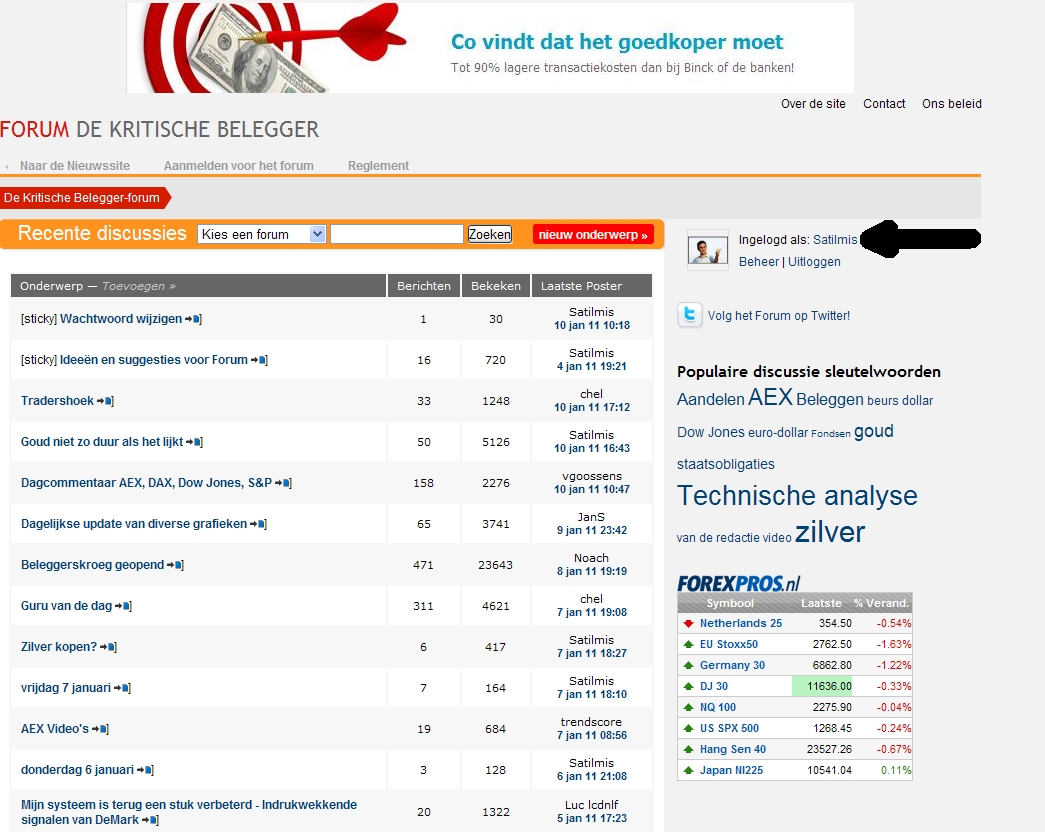

Als u zich aanmeldt genereert het systeem een wachtwoord die naar u gemaild wordt. Dit password is echter lastig te onthouden.

Via je profiel kun je dat wijzigen.

Daarvoor moet je naar de rechterbovenkant waar “Ingelogd als:” staat (zie zwarte pijl in onderstaande figuur).

Klik op je gebruikersnaam en dan kom je bij je profiel. Klik op tabblad “Bewerken” Aan het eind zie je

“Wachtwoord

Om je wachtwoord te veranderen, tik hier beneden tweemaal een nieuw wachtwoord in”

P.S. via tabblad “Mijn afbeelding” kun je ook een leuke avatar uploaden.

ING-analist Roelof Van Den Akker denkt dat Dow Jones 15% omlaag gaat.

Roelof Van Den Akker, ING’s senior technical analyst, spoke to CNBC this morning about the U.S. market. While it seems nearly everyone has gone bullish, particularly on H1 2011, Van Den Akker has gone bearish saying now is a good time to sell. He sees the DOW at a key technical level, that’s going to take it south by 15%.

We’re at least in for a short term pause after the rally, but in my opinion we’re on the brink of a correction. We’ll likely correct in Q1 to 10200 or 10000.

Around a 15% drop is what we’re expecting; everyone is bullish right now… this is the best excuse to sell stocks right now.

Nieuwe deelnemers hartelijk welkom!

Misschien is het een idee dat de deelnemers in deze draad zich even kunnen voorstellen. Hoeveel ervaring hebben jullie met beleggen en welke producten gaat jullie voorkeur naar uit?

Maak je geen zorgen om de correctie van zilver en goud.

Seasoned gold and silver investors tend not to get too rattled on price dips and in many cases use the lower prices to add to their positions, but sometimes downward swings are more difficult for newer investors or the risk adverse to stomach. With gold and silver going through a correction currently, this is a good time to analyze recent market activity and examine our reasons for remaining bullish.

As the current bull market for gold and silver continues to pick up momentum, we should expect increased volatility. We have started to see early signs of this already. By mid-fall of 2010, both gold and silver entered a mini-parabolic phase, and some of the charts, especially for silver, appeared almost vertical. Gold and silver increased 24% and 80% respectively during the course of 2010, but as I write, we have entered a correction with gold trading approximately 4% below its 2010 high and silver at 6% below. These corrections are a natural part of market activity and nothing to get overly concerned about. On November 9, the CME (Chicago Mercantile Exchange) raised its margin requirements for futures contracts for silver by $1500, and consequently, gold fell 2% and silver fell 5% during afternoon trading hours. Strong bullish sentiment means precious metals markets can occasionally overheat, and if we experience another wild swing to the upside, we should expect more rule changes from the exchanges that could result in a major correction since part of their responsibility is to contain volatility and maintain orderly markets. We should also expect prices to fall as the inevitable profit taking follows.

While these corrections can be upsetting for precious metals investors, it helps to remember James Turk’s long-term targets for gold and silver. Mr. Turk sees gold at $8000 an ounce and silver at $400 an ounce between 2013-2015. He has also confirmed that the physical market for silver remains extremely tight, so it is only natural for its price to continue to rise. And since gold and silver tend to travel in tandem, silver will take gold along for the ride upwards. Mr. Turk is well respected with those who invest in physical metals, and according to options trader Vincent Lanci of FMX Connect, James Turk has since achieved guru status within his circle due to the accuracy of Mr. Turk’s recent calls. As a result, traders now pay close attention to his predictions as well.

Whenever gold and silver have a big move to the upside or downside, investors should seek out the analysis of the likes of James Turk and check out the King World News website at http://www.kingworldnews.com. Eric King keeps a close eye on the market and typically interviews James Turk, Jim Sinclair, John Embry, or Ben Davies whenever major price action occurs. Investors can then listen to the interview or read about Mr. King’s conversation in article form on his blog. The point is to seek out information whenever prices change significantly rather than react based on fear or panic.

As Richard Russell cautions, the point of a bull market is to shake off as many investors as possible. The bull attempts to buck the greedy and the faint of heart. Don’t be one of them. If current Federal Reserve policy doesn’t change, the US could suffer a hyperinflation. When that happens, the dollar will be worthless, and you’ll be glad you didn’t sell your gold and silver.

Gaat Portugal crashen? De Portugese PSI20-index onder zware verkoopdruk.

Bernanke: banengroei nog altijd onvoldoende

WASHINGTON (AFN) – De groei van de Amerikaanse economie is niet sterk genoeg om de werkloosheid te bestrijden. Dat zei de Amerikaanse centralebankpresident Ben Bernanke vrijdag tijdens een hoorzitting in het Amerikaanse Congres.

Eerder op de dag meldde het Amerikaanse ministerie van Arbeid dat er in december 103.000 nieuwe banen bijkwamen in de Amerikaanse economie. ,,Dat is nauwelijks genoeg om de normale groei van de beroepsbevolking bij te houden en daarom onvoldoende om de werkloosheid werkelijk te verbeteren”, aldus Bernanke.

De voorzitter van de Federal Reserve gaf wel aan dat hij steeds meer positieve signalen voor de Amerikaanse economie ziet. Hij verwacht echter dat de werkloosheid nog een aanzienlijke tijd hoog zal blijven.

Om de banengroei VS in perspectief te plaatsen:

Today, the Labor Department reported that nonfarm payrolls (jobs) increased by 103,000 in December. For some perspective, today’s chart illustrates the percent increase in the number of jobs for every decade since the 1940s (the data goes back to 1939). Today’s chart illustrates that up until this millennium, the number of jobs at the end of a decade has always been at least 20% greater than 10 years prior. During the last decade, not only was that 20% plus growth not achieved, the decade actually ended with less jobs than when it began. This negative job growth is particularly noteworthy due to the fact that the US population had increased by 10% in addition to a significant increase in global wealth during the same time frame. With one year down in the current decade (see gray column), today’s chart illustrates that job growth is positive albeit only slightly so. If job growth during the current decade were to increase at the same pace as what occurred during the first year of this decade, the decade would end with an 8.7% gain in jobs (see gray dot). This is certainly better than the decade just passed, however, it is well off the 20% plus pace of decades past.

De vorm van het economische herstel, een uitgave van de Fed.

http://www.newyorkfed.org/newsevents/speeches/2011/tra110107.pdf

Weliswaar valt de totale banengroei VS tegen maar het cijfer van de vorige maand is opwaarts bijgesteld van 39.000 naar 71.000 en bovendien een sterke groei van de werkgelegenheid in de particuliere sector. Dus cijfers vallen niet echt tegen.

Banengroei VS valt tegen

07-01-2011 14:30:00 VS werkloosheid nov ongewijzigd op 9,8%

07-01-2011 14:30:00 VS aantal banen nov bijgesteld tot +71.000 van +39.000

07-01-2011 14:30:00 VS aantal banen private sector dec +113.000

07-01-2011 14:30:00 VS gemiddeld uurloon dec +$0,03 naar $22,78

07-01-2011 14:30:00 VS werkloosheid dec 9,4%; verwachting was 9,7%

07-01-2011 14:30:00 VS aantal banen dec +103.000; verwachting was +150.000 -

AuteurBerichten