Tags: daling, Dow Jones, edelmetalen, goud, goudprijs, papiergeld, staatsobligaties, zilver

Dit onderwerp bevat 85 reacties, heeft 19 stemmen, en is het laatst gewijzigd door Bluevision 13 jaren, 9 maanden geleden.

-

AuteurBerichten

-

9 december 2010 om 19:42 #link naar dit bericht

Goud gaat $150 stijgen binnen 5 weken!!!

The contact out of London has updated King World News on the massive Asian buyers which have been accumulating both gold and silver. The London source stated. A bunch of the weak hands are now on the short side of this market. We are very close to a floor because of the massive Asian buying. People have to remember these Asian buyers are now controlling the gold and silver markets, it is not the little guy.

The London source continues:

“It’s all about the bond auctions, the bond fell off a cliff. In the derivatives market you’ve got JP Morgan playing the bond market at the behest of the Fed, going long 30 years versus selling short-term paper. They buy 30 year paper and then immediately hedge themselves by selling the 30, 60 and 90 day paper. It’s how they keep interest rates down, it’s how you do it.

The only reason interest rates are not in double digits in the US is because of this game. These guys are short front month paper. If this (the bond market) actually fell much longer, JP Morgan could be wiped out, I mean they would be liquidated. The Fed cannot allow them to do that. We’re witnessing history here.

Money flowing out of bonds is going into precious metals. So what they are doing is trying to paint the tape and make it look like a double-top in gold, with silver also retreating. Open interest went up into the decline, this is a gift (the decline). Asian buyers are laughing, we’re like a cartoon to them. They cannot believe how orchestrated this is.”

Where do you see a floor on silver?

“I think to go through $27 is virtually impossible, it would be suicide. I don’t think it will even get there. They are getting very cheeky even taking it below $28. They are not going to push it below $27 because they would just lose too much physical.

All that’s happening here is the Fed is freaking out because the bond market is collapsing and they want to indicate that everything is fine, and certainly that precious metals is not your alternative. Meanwhile, the Asians will continue to buy any dip and keep adding to their position. For what it is worth, Jim Rickards is correct, the Asians are doing their buying through secret agents.”

What about gold?

“As far as the gold market is concerned, gold will be $150 higher from here within five weeks.”

Well there you have it, this London source has called these markets to absolute perfection. There is a huge floor nearby, and gold will explode $150 higher in a matter of weeks. Stay tuned as we will have more from the KWN source out of London in the days ahead.

Eric King

KingWorldNews.com23 december 2010 om 10:01 #link naar dit berichtHet International Monetary Fund heeft afgelopen dinsdag aangekondigd, dat zij de verkoop van 403.3 ton goud hebben verkocht. Analisten hadden verwacht dat dit bericht van invloed zou zijn op de goudprijs, maar niets bleek minder waar. De goudprijs bleef namelijk steken tussen de 1389 en 1390 Dollar.

27 december 2010 om 14:57 #link naar dit berichtVerkoop je goud voor april volgend jaar. Want dan (of in een van de twee volgende maanden) loopt de lucht uit de goudmarkt. De prijs van goud gaat kelderen. De gouden bubbel knapt.

Dat schrijft de econoom Mathijs Bouman op zijn blog. Hij haalt een onderzoek aan van vier Russische wetenschappers.

Ze pasten de log-periodic-oscillations-power-law-quasi-singularity theorie toe op de prijs van goud. De theorie klopt precies met de empirie, de goudprijs beweegt richting een crash.

Het kritische punt wordt ergens in het voorjaar bereikt, denken de Russen. Dan volgt de crash. Verkoop voor die tijd al je gouden munten! Verpats je juwelen! Graaf die baren goud weer op uit de tuin en gooi ze op marktplaats! Sell, sell, sell!

Bijgevoegd is het rapport van de Russische wetenschappers in pdf.

Is goud volgens u te duur en is er sprake van een goud-bubble?

Reageer ook. Aanmelden voor het forum kan via http://forum.dekritischebelegger.nl/forum/register.php

Attachments:

Goud_crasht_in_april-juni_2011.jpg

Possible_Burst_of_the_Gold_Bubble.pdf29 december 2010 om 20:19 #link naar dit berichtIk verwacht de daling van de goudprijs iets later dan april volgend jaar.

Dat het een bubble is staat buiten kijf maar zolang de Verenigde Staten maar geld bij blijven drukken en China een exportverbod op grondstoffen in stand houdt blijft er een schaarste bestaan.

Deze schaarste zal de prijs mijnsinsziens nog wel enige tijd op niveau houden.

3 januari 2011 om 20:32 #link naar dit bericht@beunhaas, ik geloof ook niet dat goud de dieperik ingaat, maar zilver lijkt me aantrekkelijker dan goud. Wat is jouw voorkeur?

Hier de vooruitzichten van James Turk: http://www.fgmr.com/outlook-for-2011.html

4 januari 2011 om 19:45 #link naar dit berichtMijn voorkeur gaat op dit moment uit naar zilver.

Maar dan wel fysiek zilver, er is een hoop ongedekt zilver op papier in omloop.(Bron: National Inflation Association)Er is dus ook net zoals goud een bubble in vorming vandaar fysiek zilver.

Maar ook hier geldt dat de schaarste van deze grondstof de prijs wel redelijk op niveau zal houden.4 januari 2011 om 21:02 #link naar dit berichtDus een instapkans in zilver bij deze correctie?

5 januari 2011 om 05:21 #link naar dit berichtAls je op langere termijn kan denken, is fysiek goud en zilver nooit mis, zolang er toestanden zijn als opkopen van de eigen schulden door de eigen nationale bank.

5 januari 2011 om 11:48 #link naar dit berichtGoudexplosie

The New Gold Rush

As confidence in global currencies wanes, the world’s appetite for gold will increase.

By Nick Barisheff

as published in onwallstreet.com

As we embark on 2011, gold continues to climb and investors are questioning its future price direction. Is gold in a bubble? Have the price gains of the last decade-which beat out stocks, bonds and several other favored asset classes- peaked? Did today’s investors miss the opportunity to buy?Since 2002, we have responded to these questions daily, as gold climbed from $275 an ounce to over $1,400. Unfortunately, most people see gold as just another dollar-based asset class to be evaluated using the same metrics as stocks and bonds, and commodities like corn and coffee. But in order to understand the benefits of buying and holding physical gold, investors must go beyond conventional economic wisdom and understand causes rather than symptoms. They need to be able to interpret the message gold is sending.

Gold has its own rules, which explain its price performance and form the foundation of what we call “the gold mindset.” This is completely different from the debt-based mindset that has prevailed since 1971, when President Nixon removed the U.S. dollar-the world’s reserve currency-from its international peg with gold. Eliminating the gold standard has resulted in anywhere from $14 trillion to $200 trillion of debt for the U.S., which now relies on a phenomenon called “Quantitative Easing” (QE) for economic survival. QE, or money printing, has triggered global currency devaluations and protectionism worries.

In this piece, we will examine four of gold’s most important rules; the irreversible trends affecting the gold price; and how the consequences of these trends will push gold higher in 2011 and beyond.

The Golden Rules

Rule 1: Gold is money, not a commodity. Gold trades on the currency desks of the major banks and brokerage houses, not the commodity desks. Central banks have always regarded gold as money, yet many investors today view it as an ordinary commodity, like pork bellies. Because none of the world’s currencies are backed by gold, it has become the anti-currency-the money of last resort impervious to Wall Street games, Main Street’s over-consumption or QE-happy Keynesians. In 2009, gold officially became money once again when central banks around the world, including those of China, India and Russia, became net buyers for the first time in nearly 20 years. We believe that central banks are preparing for a return to some form of the gold standard.

Rule 2: Gold does not rise: currencies lose purchasing power against gold. Milton Friedman-the renowned American economist-stated: “Nations are not ruined by one act of violence, but gradually and in an almost imperceptible manner, by the depreciating of their circulating currency, through excessive quantity.” That is bad news for the U.S., Canada, Britain, the Eurozone and Japan. Their currencies have lost more than 70% of their purchasing power against gold during the past 10 years. When we begin asking: “How many ounces of gold will this cost?” rather than, “How many dollars will this cost?” The shift in perspective is eye-opening.

Gold is a stable economic measure and a reliable standard by which to measure real inflation. Governments manipulate inflation figures to keep the official Consumer Price Index (CPI) artificially low, since the slightest rise can translate into billions of dollars in government-indexed pension payments to the growing number of baby boomer retirees. Today, instead of using a fixed basket of goods that represents a certain standard of living, methods such as substitution, hedonic adjustments (for estimating demand or value) and geometric weighting, are used to understate the CPI.For instance, John Williams of http://www.shadowstats.com, calculates the CPI using the original methodology. His figures show that real inflation is already at 8.5% and climbing. Since the CPI has an inverse relationship with Gross Domestic Product (GDP), understating the CPI automatically overstates GDP.

Rule 3: Gold has intrinsic value. Gold has intrinsic value because it is difficult to find, to mine and to refine. In Roman times, an ounce of gold would buy a good suit of clothes; today, the same applies. In his book, “The Golden Constant,” Prof. Roy Jastram demonstrated that gold’s purchasing power remained remarkably stable between the years of 1560 and 2007.

Rule 4: Gold is a wealth-preserving asset, not a wealth-accumulating asset. We buy and hold gold bullion to preserve wealth. We may speculate in gold stocks, exchange-traded funds, futures and options to increase wealth, but gold bullion ownership best serves the purpose of wealth preservation. This has been the case for thousands of years and will continue to be so unless governments discover a way to produce gold out of thin air, as they do fiat currencies.

Three Irreversible TrendsSince gold appears to be rising because of currency debasement (a term derived from the Roman Empire’s practice of hollowing out gold coins and filling them with base metals), we need to consider whether governments will continue to spend and whether inflation will continue to rise. Three irreversible trends indicate that this pattern will persist for years to come. They are the aging population, outsourcing and peak oil.

The world’s population is getting older, and most countries offer government-funded social programs designed to help retirees enjoy their golden years. However, an aging population means rising health care costs along with declining tax revenues. This is an unsustainable situation. In Europe, there has been rioting in the streets, as people protest retirement age hikes and cuts to benefits and services.

North American companies now outsource whatever they can with no regard for employees or communities; only the bottom line matters. It is far cheaper to hire someone in China-at 80 cents per hour with no benefits-than it is to hire someone in America-at $20 per hour, plus benefits. Without government protectionism, shareholder pressure ensures that this trend is irreversible. Without jobs, people cannot pay taxes or buy goods.

Finally, we have the serious issue of peak oil, which threatens to destroy the global economy, heavily dependent on cheap fossil fuel. Peak discovery has already occurred and we are fast approaching peak production of reasonably priced oil. Switching over to more expensive oil or to alternative fuels will have a negative impact on global GDP. This irreversible trend will fuel inflation for years to come.

The Consequences

These macro trends will result in:

• lower GDP

• systemic unemployment

• lower tax revenues

• increased money supply

• more government debt

• rising inflation

• declining currency value

• and higher gold prices.Increased government debt and money printing to service the interest on this debt are direct consequences of these three trends. Since 1971, U.S. debt has soared to $13.96 trillion from $776 billion. Boston University economist Laurence Kotlikoff disagrees with that number; he believes true U.S. debt is $200 trillion, or a staggering 840% of GDP.

As investors lose confidence in currencies, the world’s appetite for the relatively small amount of available gold will increase. There is an estimated $200 trillion in financial assets worldwide, not including real estate and derivatives. When demand for gold as a safe haven increases, there will be a transition from the $200 trillion financial assets market, to the $3 trillion gold market-much of which is owned by central banks and the world’s wealthiest families, and not for sale at any price.

Future: Too Much Money Chasing Too Little GoldThe Chinese government is encouraging its citizens to invest 5% of their savings in bullion. Central banks in China, India and Russia are scrambling to increase reserves. Investment funds and banking institutions globally are turning to gold for insurance. Meanwhile, gold discoveries are down and production costs are rising. Clearly, competition for available gold will become fierce.

Where will the price of gold go?

In 2011, if gold repeats its average five-year increase of 19%, it will climb to $1,785 per ounce. If gold repeats 2010’s projected performance in 2011, it could reach $2,010 per ounce. If the U.S. Federal Reserve unleashes more QE, gold’s price will be much higher.

Today, gold is telling us that it can protect our wealth as it has successfully done for thousands of years. In such uncertain times, it is comforting to know that bullion ownership allows for sovereignty over personal economic destiny, and can change the way we view and experience economic reality.Via Rob.

10 januari 2011 om 15:43 #link naar dit berichtEigenlijk is het de schuld van Nixon in 1971. Die heeft de goudstandaard verlaten. Dit kwam doordat hij nogal wat geld nodig had voor de oorlog in Vietnam.

Dus is hij meer geld gaan bijdrukken dan dat er goud was. Nu is het hek van de dam. Wat er nu de Amerika gebeurd is onomkeerbaar.

Op naar de HYPERINFLATIE.

Als we nu weer al het geld willen afdekken met GOUD. Waar zal de goudprijs dan naar toe gaan?

Lees ook stukje over Bretton Woods op Wikipedia.

Auteur: Rob

10 januari 2011 om 17:38 #link naar dit berichtKijktip voor vanavond: Jim Rogers en Arianna Huffington in Tegenlicht: Agenda 2011.

Maandag 10 januari 20:55 NED2

De economie flink in het rood, de politiek hopeloos gepolariseerd en de wereld weer ouderwets verdeeld. Hoogste tijd voor nieuwe inspiratie. Zoals elk kalenderjaar ging Tegenlicht ook in november en december 2010 weer op zoek naar zijn ‘tijdgeestverwanten’. Om de vooruitzichten te peilen voor het jaar 2011, en daar voorbij: het decennium ‘jaren ’10’. De speurtocht in de wereld van wetenschap, economie, futurologie en nieuwe media resulteerde in vier tegendraadse en vernieuwende doordenkers. Voorgangers naar een hoopvoller toekomst. Misschien wel pioniers van een nieuw paradigma.

Superinvesteerder en grondstoffenguru Jim Rogers ziet de wereld steeds meer worden zoals hij altijd voorspelde. Daarom is zijn laatste voorspelling uit Agenda 2009 nu wellicht actueel: ‘It is going to get worse’. Jos de Putter ontmoet oude bekende Rogers in Newark, in transit tussen twee vluchten. Rogers pendelt heen en weer tussen de VS en Azië, waar het volgens hem nu allemaal aan het gebeuren is. Europa kan hij gevoeglijk overslaan. Want hij voorspelde in 1999 namelijk al de val van de Euro. Want de Europese economieën zijn te divers, er is geen eenheid in de politiek en vooral: ‘’they are faking the numbers’.

http://tegenlicht.vpro.nl/afleveringen/2010-2011/agenda-2011.html

12 januari 2011 om 14:57 #link naar dit berichtTwee interessante stukjes over Goud getipt door Rob.

Gold Outlook 2011: Irreversible Upward Pressures and the China Effect

I know this may appear to some to be an enviable job—getting to speak about the one asset class that seems to continually out-perform all others year after year—but it is a double edged sword.

I’ve struggled to find an appropriate simile. The best I can come up with is that speaking about gold is like one of those good news bad news jokes, you know the ones—your doctor phoned with some good news and some bad news. The good news is they will be naming a new incurable disease after you.

The good news is that gold is rising in value; the bad news is—well nearly everything else about the economy.

This year we travelled to the Middle East, the Far East and South and Central America to discuss gold. The different mindsets about gold we encountered there surprised all of us. Most people in these countries see gold as the protector of wealth. In the West, we view gold as a commodity for speculation.

Western economists treat the act of buying gold as an admission of defeat and their attempts at disparaging gold’s steady rise became even more tenuous than ever this past year. Some of these disparaging opinions include:

“Financial tightening will cause commodity prices to fall.”

“Gold is in a bubble.”

“The gold stocks haven’t confirmed the gold bull.”Perhaps most desperate of all—“The economy is on the road to recovery.”

Despite these protests, gold had another remarkable year. It was up 25 percent in 2010, which marked its tenth straight annual gain.Although we are speaking about gold today, I would be remiss in ignoring silver’s performance. Silver is up 78 percent in 2010 as it is, like gold, beginning to assume its role as a monetary metal. Platinum was also up 17 percent.

When we look at a ten year chart of the US and Canadian dollars, the Euro, the British Pound and the Yuan, we see that these five major currencies have lost between 70 to 80 percent of their purchasing power against gold over this 10 year period. In truth, gold is not rising, currencies are falling in value and gold can therefore rise as far as currencies can fall.

Three Short to Mid-Term Trends

I’d like to pick up where we left off last year with a review of three dominant medium term trends that put upward pressure on the price of gold in 2010 and will likely continue to in 2011. Then I’d like to look briefly at three longer term, irreversible trends that will to put downward pressure on currencies resulting in upward pressure on gold for decades.

First, the three dominant mid-term trends we discussed last year. These are:

1. Central Banking Buying

2. Movement away from the US Dollar

3. ChinaCentral Bank Buying

In 2009, for the first time in 20 years, monetary gold, or central bank and investment buying, outpaced gold buying for industrial or jewellery purposes. In 2010 China, Iran, Russia and India’s central banks were all significant buyers as they moved cash reserves to gold.

In Q3 of 2010, Russian central bank gold holdings rose seven per cent to 756 tonnes. In 2010, the Russian Central Bank bought 2/3 of its own gold production.In December we learned that China had imported 209.7 metric tonnes of gold in the first 10 months of the year. This was a 500 percent increase over the same period of 2009 and on top of their world leading domestic gold production.

By the third quarter, India’s gold imports, both commercial and private, for the year were 624 tonnes, putting them 100 tonnes above the previous year’s total of 595 tonnes. Fourth quarter purchases could put India’s annual total over 750 tonnes.

China and Russia need to acquire gold to bring their gold reserve ratio to outstanding currency closer to Western central banks. Russia needs to acquire at least 1000 tonnes and China at least 3000 tonnes to remain on parity with the US. Chinese officials have stated publicly that China would like to acquire at least 6000 tonnes. Unofficially they have stated targets as high as 10,000 tonnes.

Movement Away from US Dollar

Last year we quoted a November 2009 story written by veteran journalist Robert Fisk claiming Russia and China along with France, were working on an agreement to trade oil with Arab states using currencies other than the US dollar. As expected, central bankers fervently denied these rumours. The US dollar has since 1973 been the only currency that oil could be traded in. This is the only reason the US has been able to amass nearly $14 trillion in debt. Loss of the petrodollar`s hegemony would have a devastating effect on the US as this is essentially the only reason foreign countries in the past needed to hold US dollars.

On November 24, 2010, China and Russia officially

quit the dollarand agreed to use each other’s currencies for bilateral trade—including oil. Official trading on Moscow’s MICEX Index began December 15th, 2010.In 2009, Robert B. Zoellick, made his well-publicized comment that, the US would be “. . . mistaken to take for granted the dollar’s place as the world’s predominant reserve currency.” And that, “. . . looking forward, there will increasingly be other options to the dollar.” In 2010 he continued hinting at a new reserve currency made up of five currencies with gold as the “reference point.” He also called for a new Bretton Woods agreement this year. Mr. Zoellick is no lunatic goldbug. He’s the President of the World Bank.

China

Last month, I was a speaker and panellist at the China Gold and Precious Metals Summit in Shanghai. I can confirm that Chinese buying, both official and public, is a major trend that is not only well in place, but may be the single most important influence on the price of gold in 2011. As I said, the Chinese see gold quite differently from the way we see it. If we are to understand gold’s price direction in 2011 and beyond I believe it is essential to understand the “mindset” the Chinese have built around gold.

Economic Mindsets and Gold

Although the forming of economic mindsets is a complex topic, I’d like to simplify how major financial mindsets are created in one sentence. What our government, our banks and financial media tell us about money is what most of us will accept as our financial mindset or financial reality. If anyone doubts the power of government economic policy to shape mass economic reality, just look at how we have changed our attitudes towards debt, saving and economic value over the past 40 years. Our current debt based mindset began to form the day the US dollar, the worlds reserve currency, was removed from its final international peg with gold in 1971.

Different Attitudes about Gold

Although the West shares many common economic principles with the East, as the capitalist banking systems are similar, there is one area where there is a clear distinction—this is how Easterners view the role of gold as money.

Western governments fear gold. It restricts their ability to create currency

In the West, governments borrow and encourage their constituents to follow their example. Banks encourage us to borrow for everything from vacations to widescreen televisions made in China. They tell us we are “stimulating” the economy through consumption. Generally speaking, the investing public in the West sees gold as a wealth gaining asset to be traded like stocks and bonds. This is why Westerners are constantly fretting about the price of gold in currency terms.

The Chinese government, on the other hand, respects gold. This is evident by the laws they have passed to facilitate mining and private gold ownership. China currently leads the world in gold production.

The government encourages the public to put 5 percent of their savings—yes they encourage savings—into gold. This is significant because the Chinese can save up to 40 percent of their annual salary. In the West, most middle class families are lucky to break even. The Chinese see gold as a wealth preserving asset that will weather all seasons. This is the difference that I believe anyone who wishes to fully understand gold’s rising price must comprehend. Inhabitants of older countries, who have lived through the destruction of an inflation fuelled currency crisis, do not need to be reminded that gold is the most effective hedge against inflation and a currency crisis.Former CEO of Newmont Mining, Pierre Lassonde also feels that it will be buying by the Chinese public that will eventually propel gold prices into the stratosphere.

Three Irreversible Trends

Clearly, the three medium term trends we noted last year are still firmly in place. Now I’d like to look at three longer irreversible trends that I believe will affect the price of gold and currencies for decades. These are:

1. The aging population.

2. Outsourcing

3. Peak oilThe Aging Population

The aging population is a combination of a population that is living longer and the “pig in the python” effect of a huge tidal wave of “baby boomers” born between 1946 and 1963 who are just starting to enter retirement age. As people age, they spend less and downsize. GDP and tax revenues are reduced and a much smaller workforce follows the baby boomers so this is a triple whammy. This problem is universal. In China, it is further exacerbated by their one child per couple policy. Governments will have no choice but to create more currency and further debase it.

Outsourcing

Outsourcing has almost entirely destroyed the manufacturing sectors of many first world countries like the US and Canada and much of Europe. The Chinese worker who built your IPhone made $287 a month; this was after a well-publicized raise. The West simply can no longer compete with these labour costs. The United States was the world’s largest manufacturer after WWII and has driven the world’s economy ever since. However, the US consumer can no longer buy things as they lose their jobs. As factories move off shore the high unemployment becomes systemic. Without jobs, the GDP and the tax revenues of the US fall. The mountain of federal, state and municipal debt will become even harder to service and the government will be forced to go even deeper in debt and to further debase its currency.

Peak Oil

Peak oil is the point at which the maximum rate of global petroleum extraction is reached, after which the rate of production enters terminal decline. This has already happened in the US, Alaska and the North Sea. In the next few years Mexico will become an importer of oil and the US will lose its third largest supplier. Our fragile, highly indebted economy relies on this land based cheap oil to continue and it cannot withstand the shock of transitioning to more expensive alternatives. In September of 2010 a German military think tank reported that the German government is taking the threat of peak oil seriously and preparing accordingly. Numerous studies around the world have concluded that we are very close to peak oil production, which will be accelerated due to gulf drilling bans.

This will lead to higher price inflation for most goods. This will be another blow to the fragile US economy, which currently pays less for oil and gas than any of the first world countries. When added to the effects of the waning strength of the petrodollar the results will be devastating.

May I remind you that if China, which currently has one tenth the number of cars per capita as Americans, was to reach par with the US, we would need, by one estimate, seven more Saudi Arabia’s to meet their needs.

These three mega trends will continue to lower the GDP, lower the tax revenue, create higher trade deficits, create higher unemployment, resulting in the need for further currency creation. This will cause inflation to rise as currencies depreciate in value and create higher universal debt. All of this means the gold price will continue to rise.

Competition for the World’s Gold

Finally, as a direct result of world-wide debt and currency debasement, more people will be competing for the world’s available gold. We discussed peak oil, but gold is also reaching a peak as fewer and fewer new deposits are being found. Smaller, lower grade deposits with none of the “economy of scale” benefits of larger deposits are being put into production out of desperation. Mine supply has been in a decline since 2000.

As safe haven demand accelerates, there will be a transition from the $200 trillion of financial assets to about the $3 trillion of above ground gold bullion. Of the $3 trillion of above ground gold bullion about half is owned by central banks and half is privately held. The privately held gold is largely held by the world’s richest families and is not for sale at any price. The central banks are now net buyers. If the world’s pension funds and hedge funds moved only five percent of their assets into gold, which these days seems quite conservative, gold would trade above $5,000.

So in conclusion, I will say that without any new financial crisis, both mid-term and long term trends are in place to ensure gold and silver will continue rising through 2011 and well beyond. For those of you who are looking for a prediction…last year at the Empire Club, I forecast that the price of gold to be between $1300 and $1500 at the end of 2010. We ended up right in the middle at $1405. For 2011, I recently forecast it may climb to $1,700 to $2000 per ounce based on the last five years performance and the factors I have presented today.

I encourage you to follow the example of those who know how devastating a currency crisis can be and buy gold to protect wealth and not treat it as speculation. I’d like to close with a quotation that seems to put all of this into perspective. It comes from Norm Franz’s appropriately titled book, Money and Wealth in the New Millennium. He said,

“Gold is the money of kings; silver is the money of gentlemen; barter is the money of peasants; but debt is the money of slaves.”Thank you.

12 januari 2011 om 15:05 #link naar dit berichtThe “Money Supply” with a Gold Standard 2 : 1880 – 1970

by Nathan Lewis – New World Economics

Originally published January 11th, 2011Last week, we were looking at how gold standard systems work. We used the example of the United States, which, from 1789 to 1860, had a libertarian “free banking” system. Anyone could issue currency, but it had to be pegged to gold. This “gold peg” was a value peg. It had nothing to do with gold mining, or the gold reserves of banks, or imports and exports of gold. Does gold mining alter the value of gold? Essentially no, because annual gold mining production is a small fraction — about 2% — of existing world gold supply. Does importing and exporting gold change the value of gold? Not unless there are some sort of restrictions on importing and exporting, which is rare, and hard to enforce even if it exists. Gold is the same value everywhere. Does the fact that a bank owns or does not own gold change the value of gold? Nope. It’s the same value no matter who owns it. So you see, none of these factors have much effect on the value of gold. And if a banknote’s value is pegged to gold — via the adjustment of supply — then obviously these factors have little effect on the value of banknotes.

The fact of the matter is, during the “free banking” period, nobody actually knew what the “money supply” was. In 1859, the Hodges Genuine Bank Notes of America listed 9,916 notes issued by 1,356 banks. Yes, there were 1,356 banks all issuing their own homegrown currency in those days, all of it linked to gold. Actually, there were more than 1,356 banks, because Hodges missed dozens if not hundreds of banks! Banks were opening and closing all the time. Do you see? Not only did nobody know the total amount of banknotes in issuance (except for some vague statistics), nobody even knew how many banks there were issuing currency. Think about that. So how was the money supply determined in those days? All of these 1,356+ banks had the same operating mechanism, which was a gold value peg maintained via the adjustment of supply. When the value of banknotes was a little low compared to its gold peg, the supply of banknotes was reduced. When people were happy to accept larger issuance of banknotes, without redeeming them for gold, in other words when the value of banknotes was higher than the gold peg, then the supply of banknotes increased.

January 2, 2011: The “Money Supply” With a Gold Standard

August 26, 2007: How To Operate a Gold Standard

August 19, 2007: Gold Standard FallaciesUnfortunately, today we have all sorts of the stupidest imaginable ideas floating around, whereby a “gold standard” is a system by which the amount of money in circulation is determined by gold mining, or the “current account balance,” or that a gold standard means a “100% gold reserve ratio” or absolutely no change in the “money supply” whatsoever, some such thing. Anyone with the briefest understanding of historical monetary statistics — this includes you if you read last week’s item — can see immediately that this is complete baloney. The next thing you should realize is that 99% of academic economists including Ben Bernanke and also 95% of gold standard advocates including Murray Rothbard — also have no idea whatsoever how real gold standard systems operated, in real life during the period 1789-1971. What this means is that, after spending 20 minutes to read last week’s item, you now know more about this than 95%+ of the so-called “experts.” Do you see now why I say that today’s understanding of these matters is appalling? On the other hand, you can now be a World Expert with about 45 minutes of work. Which is sort of fun, in a way.

Let’s continue our story in 1880. In 1863, the National Bank Notes system was introduced in the United States. Banks that wanted to issue currency had to register with the Office of the Comptroller of the Currency, an agency of the U.S. Treasury. There were still thousands of these National Banks — 3,438 National Banks in May 1890 — so it was still a libertarian sort of system. However, now we have system-wide statistics on the total banknotes outstanding. The dollar floated vs. gold from 1861 to 1879, so 1880 is a good place to restart our tale of how the gold standard system operated in the United States. The National Banks themselves didn’t hold gold reserves for the most part, but rather U.S. Treasury obligations. The gold reserve of the National Bank system was the U.S. Treasury itself.

Here is some information on the National Bank system from the annual reports of the OCC:

http://fraser.stlouisfed.org/publications/comp/

The St. Louis Fed has all kinds of wonderful historical stuff. You used to have to go to the library for this sort of thing. I did a lot from microfilm! Ugh.

Unfortunately, I don’t have good statistics on U.S. Treasury gold holdings from 1900 to 1913. I only have 1905 and 1910. So, the intervening years are linearly extrapolated. If you have these numbers, let me know.

Let’s review first the history of the dollar.

The “dollar” was originally a European silver coin called the “thaler.” It originated in 1518. This became the Spanish silver “dollar,” which became the template for the U.S. dollar when the dollar was defined in 1792. So, the idea of the “dollar/thaler” goes waaaay back.

Except for a minor adjustment in 1834, the dollar’s value was unchanged until the Roosevelt devalutation in 1933. We can consider the entirety of the 1789-1932 period as having a dollar pegged to gold at $20.67/oz. There was a lapse during the Civil War, and also some business around the War of 1812. After the Roosevelt devaluation, the dollar was pegged at $35/oz., until 1971. However, there were some lapses during this time too, especially during World War II.

Here you can see the Civil War devaluation and return to the gold standard, the 1933 devaluation, and the floating currency period after 1971.

This shows the WWII “lapse” in the gold standard — the U.S. wasn’t quite off gold, but not quite on it either, it was all a little fuzzy, hey, there was a war going on — and the return to the $35/oz. peg around 1952, after the “Fed Accord” of 1951. The dollar sank to about $43.25/oz. at its lowest point in 1948, which is to say that it took 43.25/35=23.5% more dollars to buy an ounce of gold, or in other words the dollar’s value fell by 19%. Not really that big a deal, as long as it didn’t get out of hand.

There you go. The pink bars are base money (not including gold coin), basically banknotes and bank reserves. The green bars are the total amount of gold held by the U.S. Treasury, in terms of dollars. You can see a big jump in gold reserves in 1934, because that’s when they were revalued at $35/oz. instead of $20.67/oz. The data comes from Milton Friedman A Monetary History of the United States, “high powered money” minus gold coin, which comes from the Federal Reserve’s Banking and Monetary Statistics. The base money figues after 1918 come from the St. Louis Fed.

During this period, base money expanded by 90x. If you adjust for the 1933 devaluation, the expansion in the “gold value of the money supply” is 53x. Does that sound to you like “no expansion in the money supply”? During this period, 1880-1970, the total amount of gold in the world rose by 6.51x. So you see, the money supply with a gold standard has nothing to do with gold mining, imports or exports of gold, the current account balance, “no expansion in the money supply,” “100% reserves” or some other stable reserve ratio, or all the other stupid things you hear about all the time.

24 januari 2011 om 17:18 #link naar dit berichtGoud-en Zilverstorm op komst met twee zonnen in 2012.

Earth could be getting a second sun, at least temporarily.

Dr. Brad Carter, Senior Lecturer of Physics at the University of Southern Queensland, outlined the scenario to news.com.au. Betelgeuse, one of the night sky’s brightest stars, is losing mass, indicating it is collapsing. It could run out of fuel and go super-nova at any time.

When that happens, for at least a few weeks, we’d see a second sun, Carter says. There may also be no night during that timeframe.

The Star Wars-esque scenario could happen by 2012, Carter says… or it could take longer. The explosion could also cause a neutron star or result in the formation of a black hole 1300 light years from Earth, reports news.com.au.

But doomsday sayers should be careful about speculation on this one. If the star does go super-nova, Earth will be showered with harmless particles, according to Carter. “They will flood through the Earth and bizarrely enough, even though the supernova we see visually will light up the night sky, 99 per cent of the energy in the supernova is released in these particles that will come through our bodies and through the Earth with absolutely no harm whatsoever,” he told news.com.au.

In fact, a neutrino shower could be beneficial to Earth. According to Carter this “star stuff” makes up the universe. “It literally makes things like gold, silver – all the heavy elements – even things like uranium….a star like Betelgeuse is instantly forming for us all sorts of heavy elements and atoms that our own Earth and our own bodies have from long past supernovi,” said Carter.

UPDATE: To clarify, the news.com.au article does not say a neutrino shower could be beneficial to Earth, but implies a supernova could be beneficial, stating, “Far from being a sign of the apocalypse, according to Dr Carter the supernova will provide Earth with elements necessary for survival and continuity.”

http://www.huffingtonpost.com/2011/01/20/two-suns-twin-stars_n_811864.html

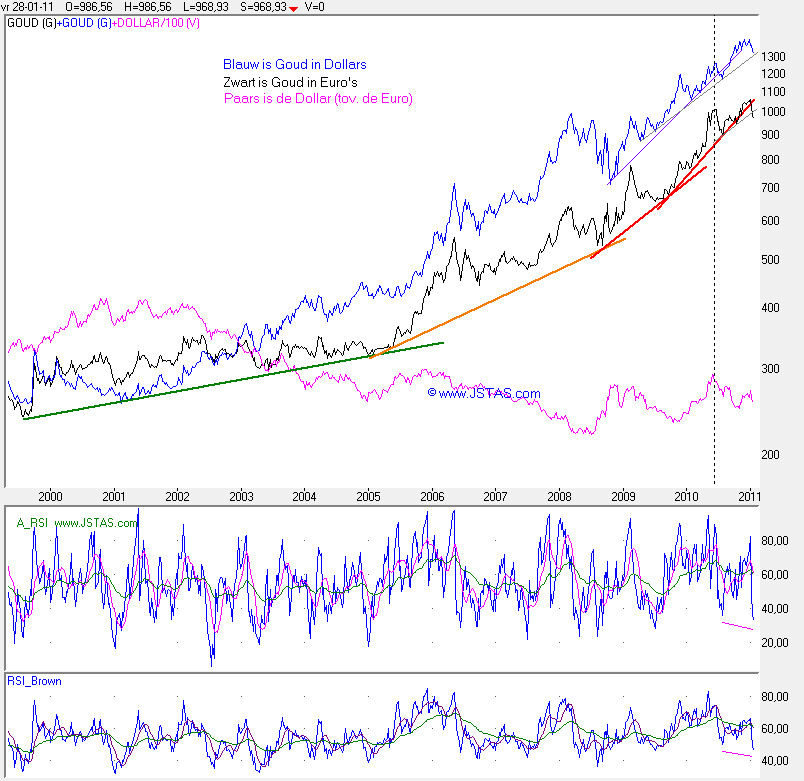

27 januari 2011 om 20:06 #link naar dit bericht#Goud fors lager, iemand een idee?

29 januari 2011 om 20:02 #link naar dit berichtDoor de plotse stijging na het sluiten van de Europese beurzen, hoor ik sommige mensen jubelen. Daarom heb ik, hoewel technische analyse zijn waarde grotendeels verliest in een sterkt gemanipuleerde markt, eens vlug een analyse gemaakt op basis van mijn excelbestand.

Twee voorafgaande opmerkingen. De analyse is gemaakt in euro en niet in dollar. Op fundamenteel vlak denk ik dat je best deze daling uitzweet of zelfs gebruikt om bij te kopen. Op het ogenblik van schrijven, is de datum 29/01, maar de plotse stijging heb ingevuld als zijnde de slotkoers van 31/01. Uiteraard zal die koers een andere waarde krijgen binnen een paar dagen, maar ik heb geen glazen bol om even de juiste slotkoers vooraf te bepalen.

Voor goud in euro kunnen wij kort zijn. Afgezien van de fundamentele analyse en enkel afgaand op de technische analyse zou je nu geen goud meer mogen bezitten. Anders is het huilen met de pet. Van alle kanten bekeken, staan alle signalen op rood.

Het Optie Spectrum, een voorspellende contrair indicator is van op vier-dagen-basis van 2 naar 3 gesprongen. Dat is een duidelijke waarschuwing dat de daling technisch nog niet afgewerkt is.

Voor zilver is het iets positiever, maar ik zou toch maar opletten, vanuit technisch oogpunt bekeken. De koers zit in de wolk van de Ichimoku grafiek, maar je kan mooi zien dat de onderste lijn die de wolk vormt, als weerstand heeft gefungeerd.

Op basis van het 5-13-62 EMA systeem voor zilver, zien wij dat de EMA13 steun vindt op de EMA62 … terwijl de koers weerstand vindt bij dezelfde EMA62. Dezelfde grafiek voor goud is veel negatiever (niet afgebeeld). De koers nadert al de EMA200 terwijl de EMA5 en de EMA13 al mooi onder de EMA62 zijn gekoerst. Als wij de traderstheorie van dit systeem mogen geloven, nadert er bijna een mooie instapkans voor zilver … short. Enkel de EMA13 moet nog onder de EMA62 komen.

Ikzelf heb geen tradingposities in goud en zilver, maar ik behoud mijn lange termijn positie in goud en zilver op basis van fundamentele analyse.

Attachments:

Technische_analyse_goud01.jpg

Technische_analyse_zilver01.jpg

Technische_analyse_zilver02.jpg

Technische_analyse_zilver03.jpg30 januari 2011 om 16:57 #link naar dit berichtEen BackTest gedraaid op zilver over 26 jaar zou een winst zijn behaald van € 1.636,52 negatief met het handelssysteem 5/13/62

Goud komt op een verlies van € 2.560,56

Voor het handelen van grondstoffen heb je dus een ander handelssysteem nodig. Wat je soms en dat is best wel vaak ziet dat mensen een systeem gebruiken geschikt voor het handelen op een index gebruiken voor alles dus grondstoffen, spots en aandelen. Dit laatste wordt robuust genoemd probleem is dat robuust niet bestaat er bestaat geen systeem wat overal en op alles werkt. Hoe langer de tijd een BackTest loopt hoe platter de uitkomst. Hoe meer je optimaliseert wat ook wel "Curve fitting" wordt genoemd hoe meer je tot de conclusie komt dat handelssystemen niet werken.

Voor grafieken en BackTest is gebruik gemaakt van ProRealTime(PR) dit is gratis EOD Bij Binck is een Lite RealTime versie beschikbaar voor € 29.50 per maand. Voor beleggers welke meer dan 20 opdrachten doen per maand bij Binck is deze versie gratis (Kick Back (dus 20 opdrachten en meer is Lite gratis minder is rekening)). Voor A Prospects (belegd vermogen meer dan € 100.000) is Lite (lees ChartNet) gratis bij Binck. Bij ToDay Brokers is Lite gratis voor beleggers met een vermogen meer dan 100.000 en A Accounts. ChartNet is het zelfde als PR. Alle HandelsSystemen genoemd en vermeld zijn beschikbaar en kunnen worden gebruikt in de EOD versie en de RealTime versie.

http://www.prorealtime.com/nl/

Attachments:

@.jpg30 januari 2011 om 17:31 #link naar dit berichtZilver

http://stockcharts.com/h-sc/ui?s=$SILVER&p=d&b=5&g=0&id=p76117352780De Wolk is dun. Elke indicator (d.w.z. Kijunu,Tenkan,Senkou) welke in de wolk noteert noopt tot het sluiten van een bestaande positie.

Koers is onder Tenkan. Koers is onder Kijun. Tenkan is onder Senkou. Chikou is onder de koers.Patroon is een Jigoku ni kantan ni

Er kan een countertrend komen tot 29.50

Het geprojecteerd koersdoel is 28.36

Opvallende grafiek Intel:

Intel heeft een negatief projectie koersdoel de Senkou is negatief.

http://stockcharts.com/h-sc/ui?s=INTC&p=d&b=5&g=0&id=p76117352780Wolk grafieken gemaakt met StockChart welke gratis d.w.z. zonder kosten te gebruiken is

http://stockcharts.com/freecharts/

30 januari 2011 om 20:13 #link naar dit bericht

30 januari 2011 om 20:13 #link naar dit bericht

-

AuteurBerichten

Je moet ingelogd zijn om een reactie op dit onderwerp te kunnen geven.